Founded in 1997, the Global Reporting Initiative (GRI) emerged from a collaborative effort between the United Nations Environment Programme (UNEP) and the Coalition for Environmentally Responsible Economies (CERES). The urgent need to develop a uniform framework that organizations all over the world could use to transparently communicate their sustainability efforts and impacts gave rise to this initiative.

GRI’s primary objective is to bolster transparency and accountability among organizations regarding their economic, environmental, and social activities. By providing a standardized framework, GRI enables companies to consistently report their sustainability performance, making it easier for stakeholders—including investors, customers, and regulatory bodies—to understand and evaluate these impacts. This consistency is crucial for comparing sustainability efforts across different industries and regions, thus fostering a more informed and responsible global business environment.

Over the years, GRI has become synonymous with best practices in sustainability reporting. Thousands of organizations in more than 100 countries have now adopted its standards, making them the most widely used in the world. By adhering to GRI standards, organizations can improve their sustainability performance, build trust with stakeholders, and contribute to the broader goal of sustainable development.

Organizations can navigate the sustainability reporting process with the help of three main categories of GRI Standards, each serving a distinct purpose.

The Universal Standards form the cornerstone of all GRI reporting. These standards address fundamental aspects that are relevant to any organization, regardless of its industry or location. They consist of key elements such as governance structures, strategic planning, and management approaches. Governance standards ensure that organizations have sturdy systems in place to oversee their sustainability efforts. Strategy standards guide organizations in aligning their sustainability goals with their broader business objectives. Management approach standards provide a framework for how organizations should implement and manage their sustainability initiatives. These universal standards ensure that all reporting is grounded in a consistent and reliable foundation, paving the path for transparency and comparability across different entities.

Since the release of the revised GRI Universal Standards in October 2021, which became effective for reporting periods starting on or after January 1, 2023, there have been no further updates or changes to these standards. The 2021 revision was a major rewrite, introducing a new structure and enhanced focus areas, including human rights and due diligence. Organizations are expected to align their sustainability reporting with these updated standards to ensure transparency and accountability in their disclosures.

Sector standards are designed to cater to the unique characteristics and challenges of specific industries. Each sector has its own distinct environmental, social, and economic impacts, and these standards offer tailored guidance to address those sector-specific issues. For example, the agriculture sector might focus on biodiversity and water usage, while the manufacturing sector could emphasize energy consumption and waste management. Financial services might need to report on investment impacts and ethical considerations. GRI provides sector-specific guidelines to ensure the sustainability reports accurately reflect the organization’s operations within its industry. This adaptive approach helps organizations identify and address the most pressing sustainability issues that they face.

GRI is expanding its Sector Standards to provide industry-specific guidance. For instance, we anticipate the release of new standards for the banking, insurance, and capital markets sectors in late 2025.

These planned updates aim to enhance the relevance and comprehensiveness of the GRI Standards, ensuring they remain aligned with evolving sustainability challenges and stakeholder expectations.

The topic standards entail specific areas of sustainability, offering detailed guidance on a wide range of issues. These standards allow organizations to report in a broad-based manner on specific topics such as climate change, human rights, labor practices, anti-corruption measures, and many others. Each topic standard outlines the key disclosures and metrics that organizations should report on to provide a complete picture of their performance in that area. For instance, the climate change standard would guide organizations on how to report their greenhouse gas emissions, energy use, and efforts to reduce climate impacts. Human rights standards would cover practices related to fair treatment, non-discrimination, and worker safety. By focusing on these critical issues, topic standards help organizations provide detailed and meaningful disclosures that address the concerns of various stakeholders.

We anticipate revising or under-revising all existing GRI Topic Standards by the end of 2025. Key areas of focus include:

Development of New Topic Standards

The GRI is also exploring new topic standards to address areas not currently covered, such as

· Cybersecurity and Data Privacy: Recognizing the growing importance of digitalization and data protection, research into developing standards for these topics is prioritized for 2024.

· Payments to Governments: Reporting on payments and contractual arrangements with governments will be included in the economic impacts project.

Together, these three categories of GRI Standards offer a deep-rooted framework that organizations can use to report on their sustainability performance in a structured and consistent manner. They ensure that all relevant aspects of an organization’s operations are covered, providing a well-balanced view of their sustainability efforts and impacts.

The GRI Standards offer a range of features and benefits that make them a valuable tool for organizations committed to sustainability reporting. Here are some key aspects:

Multi-stakeholder Engagement: The development of GRI Standards involves input from a diverse array of stakeholders, including businesses, civil society organizations, labor unions, and academic institutions. This inclusive process ensures that the standards reflect a wide range of perspectives and interests, making them reliable and widely accepted. The involvement of multiple stakeholders also helps in identifying and addressing the most relevant sustainability issues, which enhances the credibility and acceptance of the reports.

Extensive Coverage: GRI Standards embrace a broad spectrum of sustainability topics, covering economic, environmental, and social dimensions. This range of coverage ensures that all significant aspects of an organization’s operations are reported, providing a thorough overview of its sustainability performance. This extensive framework allows organizations to address all relevant sustainability issues, from greenhouse gas emissions to labor practices and community impacts.

Materiality Focus: A key principle of the GRI Standards is materiality, which involves identifying and reporting on the sustainability issues that are most significant to an organization and its stakeholders. This focus ensures that the reports are relevant and meaningful, addressing the most critical impacts and risks. By concentrating on material issues, organizations can provide stakeholders with valuable insights into their most significant sustainability challenges and achievements.

Enhanced Transparency: Transparency is a key building block of the GRI Standards. Organizations are required to disclose their sustainability information in a manner that is clear, accurate, and accessible. This openness helps build trust with stakeholders, as it allows them to see the organization’s true sustainability performance. Transparent reporting also facilitates better decision-making by providing stakeholders with reliable information.

Continuous Improvement: The GRI framework encourages organizations to continuously improve their sustainability performance. By setting goals, tracking progress, and regularly reporting on their achievements, organizations can drive ongoing enhancements in their sustainability practices. This continuous improvement approach helps organizations stay ahead of emerging sustainability issues and trends, ensuring that they remain responsive and proactive.

Overall, the features and benefits of GRI reporting make it an essential tool for organizations seeking to enhance their sustainability performance and accountability. Through multi-stakeholder engagement, extensive coverage, materiality focus, enhanced transparency, and continuous improvement, GRI Standards help organizations address their sustainability challenges effectively and communicate their efforts and achievements to stakeholders.

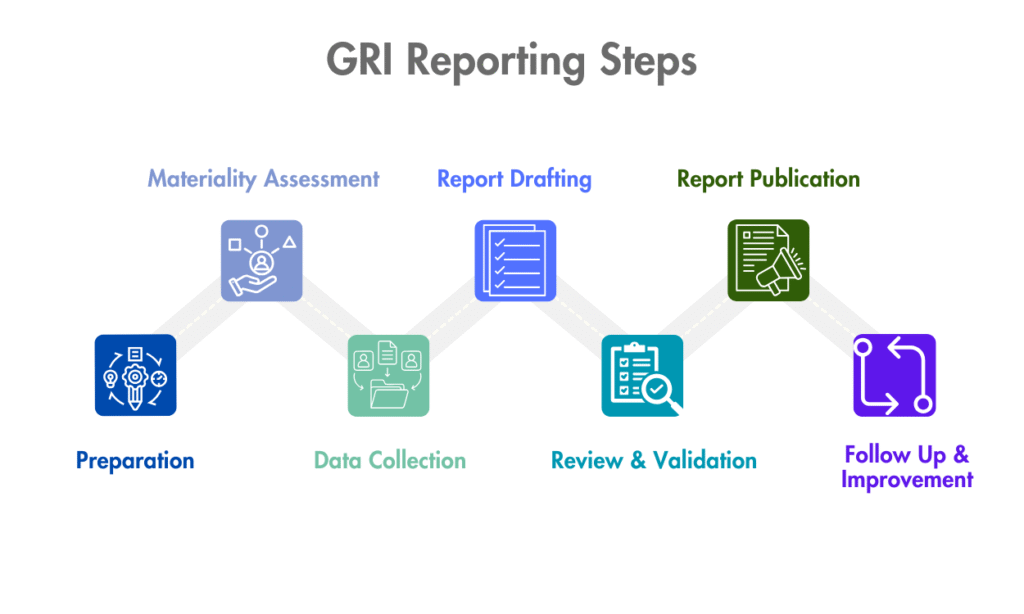

The GRI reporting process is structured to guide organizations through the systematic preparation and publication of their sustainability reports. This process ensures that the reports are all-encompassing, accurate, and aligned with stakeholder expectations. Here are the detailed steps involved:

The first step in the GRI reporting process involves identifying key stakeholders and understanding their concerns and expectations. This step is crucial for defining the scope of the sustainability report. Organizations need to determine which areas of their operations will be covered and ensure that the report addresses the interests of all relevant stakeholders, including employees, customers, investors, and local communities.

Conducting a materiality assessment is the next step after identifying the stakeholders. This involves identifying and prioritizing the sustainability topics that are most significant to the organization and its stakeholders. The materiality assessment ensures that the report focuses on the most critical issues, offering helpful details about the areas that have the greatest impact on the organization and its stakeholders.

After determining the key topics, the organization must gather relevant data. The process involves collecting quantitative and qualitative information from both internal and external sources. Accurate and comprehensive data collection is essential for creating a reliable sustainability report. Organizations may need to gather data on various aspects, such as energy consumption, greenhouse gas emissions, labor practices, and community engagement.

With the data in hand, the organization can begin drafting the sustainability report. This process involves compiling the collected information and presenting it in a structured format. The report should include an overview of the management approaches for each identified topic and detailed performance data. Clear and concise writing is essential to ensuring that the report is understandable and informative for all stakeholders.

Before finalizing the report, it is important to review and validate the information to ensure its accuracy and completeness. This step often involves seeking feedback from stakeholders and internal reviewers. By incorporating this feedback, organizations can enhance the credibility and reliability of their reports. The validation process may also include impartial external party assurance to verify the accuracy of the reported data.

Once the report is reviewed and validated, it is ready for publication. Organizations should make the final report accessible to stakeholders through various channels, such as their website, social media, and printed copies. Effective communication ensures that the sustainability report reaches all relevant audiences, enabling them to understand the organization’s sustainability performance and efforts.

The reporting process does not end with the publication of the report. Organizations should continuously track their progress against the goals and commitments outlined in the report. This ongoing monitoring allows them to identify areas for improvement and make necessary adjustments to their sustainability strategies. Regular reporting and follow-up ensure that organizations remain accountable and committed to their sustainability objectives.

By following these steps, organizations can produce high-quality sustainability reports that effectively communicate their sustainability performance and engage with their stakeholders. This structured process helps organizations build trust, demonstrate accountability, and drive continuous improvement in their sustainability practices.

GRI Standards are essential as they offer a structured and consistent approach to sustainability reporting. This standardization encourages accountability and transparency, making it easier for stakeholders to compare and evaluate the sustainability performance of different organizations. By adhering to GRI Standards, organizations can ensure that their sustainability reports are thorough, reliable, and aligned with global best practices. This helps reduce negative impacts on the environment, society, and business operations, ultimately contributing to a more sustainable world.

The GRI Standards, ESRS (European Sustainability Reporting Standards), and SASB (Sustainability Accounting Standards Board) frameworks are interconnected yet serve distinct purposes within the realm of sustainability reporting. The GRI Standards aim to provide detailed information about how a company affects the environment, society, and governance from the viewpoint of various stakeholders, highlighting what is important for society and the environment. Conversely, the ESRS aligns with the European Union’s Corporate Sustainability Reporting Directive (CSRD), incorporating double materiality to address both the company’s impact on society and the financial implications of sustainability risks. Meanwhile, SASB Standards emphasize financially material ESG factors relevant to investors within specific industries, aligning with the principles of financial reporting. Even though they focus on different things, these frameworks can work well together: GRI offers a wide view that considers all stakeholders; ESRS includes rules and looks at both financial and non-financial impacts; and SASB gives specific ESG metrics for each industry that are important to investors. Together, they create a comprehensive reporting ecosystem that addresses the needs of multiple stakeholders, from investors to regulators and the broader public.

If an organization is already reporting according to the GRI Standards, aligning with ESRS and SASB can be relatively manageable, though not without challenges. The GRI Standards provide a comprehensive framework for disclosing a wide range of ESG impacts, which already covers many of the key areas required by both ESRS and SASB. For example, GRI’s focus on the effects on all stakeholders and detailed ESG data matches the ESRS’s emphasis on double materiality, allowing companies to use their current GRI reports to meet ESRS requirements. However, ESRS introduces more stringent and sector-specific reporting requirements, necessitating additional data collection and alignment with EU regulations. On the other hand, SASB focuses on financially material ESG issues specific to industry sectors, requiring a more targeted, investor-centric approach than GRI. While GRI provides a strong foundation for general ESG reporting, SASB demands a deeper dive into sector-specific metrics that are financially material, potentially requiring additional data integration and alignment. So, even though organizations that already use GRI for reporting are in a good place to adjust to ESRS and SASB, they might still need to improve how they gather data and pay more attention to financial importance and specific industry metrics to meet all requirements.

Despite its numerous benefits, the GRI framework has some limitations. Since GRI is a voluntary framework, not all organizations choose to adopt it, which can lead to inconsistencies in sustainability reporting and make it difficult to compare reports across different entities. Additionally, the complexity of GRI Standards may require significant resources and expertise to implement effectively, which can be a barrier for smaller organizations or those with limited sustainability experience. Furthermore, without government intervention or regulatory enforcement, GRI lacks the authority to mandate compliance or penalize organizations that fail to report accurately. This reliance on voluntary adherence can limit the overall effectiveness and reach of the GRI framework.

Sustainability reporting might undergo a turbulent trajectory in 2025; nevertheless, it remains a bottom-line element of corporate transparency and accountability.

The GRI standards serve as an internationally recognized benchmark that continues to guide organizations toward comprehensive and actionable disclosures.

Organizations that choose to adopt GRI’s structured approach can still communicate their environmental, social, and economic impacts competently, ensuring they meet ongoing stakeholder expectations or regulatory demands while coping with industry-specific challenges. The path of sustainability reporting involves continuous adaptation and overcoming inherent limitations; organizations leveraging the standardized GRI framework can position themselves to effectively manage risks and capitalize on emerging sustainability opportunities. Ultimately, GRI standards, which are still widely adopted and aim for ongoing evolution, underscore their significant role in molding a transparent and sustainable global business environment.