The double materiality assessment is not as overwhelming as it may seem; all it requires is proper guidance to navigate the process with confidence, whether your DMA is mandatory under the CSRD or you are voluntarily proceeding to this step before your ESG report.

So, what is a double materiality assessment exactly? In essence, it is a dual approach to sustainability tracking that evaluates both how your business impacts the environment and society and how sustainability issues financially affect your organization. On a legal note, the double materiality assessment process is a regulatory requirement under the European Sustainability Reporting Standards (ESRS), making it essential for your CSRD compliance.

But even if you are an ESG beginner, not yet in scope for CSRD, and mostly reporting using GRI, it is still worth it, as it turns your ESG into a management system you run and future-proofs you for what’s expected next. You get to keep the credibility of impact reporting but also get a clear bridge to business risk/opportunity and strategy.

This guide walks you through a simple step-by-step on how to conduct your first ESG double materiality assessment and turn your findings into strategic decisions.

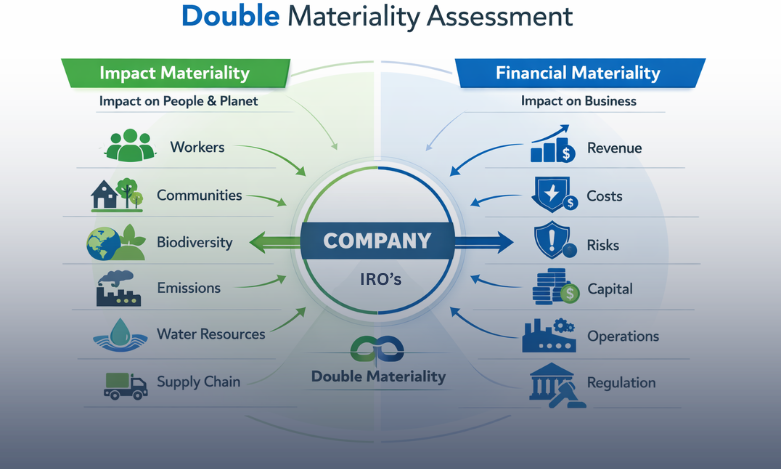

A double materiality assessment evaluates sustainability matters from two distinct yet interconnected viewpoints. Mathematically speaking, double materiality represents the union of impact materiality and financial materiality. A sustainability matter qualifies as material if it meets the threshold from either perspective or both. You don’t need overlap between the two dimensions for a topic to require disclosure.

This approach differs fundamentally from single materiality, which focuses solely on how sustainability issues affect your financial performance. Traditional assessments would consider how climate change disrupts your supply chain but ignore how your operations contribute to it. Double materiality corrects this one-sided view. According to investor surveys, 75% of investors stated that materiality assessments should include external company impacts.

Impact materiality operates from an inside-out perspective. You assess how your business activities affect people and the environment across your value chain. This evaluation considers scale (how grave or beneficial the impact is), scope (how widespread), and, for negative impacts, remediability (whether the harm can be reversed). Potential impacts also factor in likelihood and time horizon. Take the case of workplace fatalities, which would be considered severe given their irremediable character.

Financial materiality operates from an external viewpoint. You examine how sustainability factors create risks or opportunities affecting your financial performance, position, cash flows, or cost of capital. These assessments consider both the likelihood and magnitude of potential financial effects across short-, medium-, and long-term horizons.

Companies across sectors demonstrate double materiality in practice. UnitedHealth Group invested in workplace wellness programs, which reduced absenteeism and healthcare costs (financial materiality) while improving employee physical and mental well-being (impact materiality). Banks reviewing lending portfolios to avoid financing environmentally harmful activities create positive environmental impacts while managing lending risk. Such initiatives can lead to a better public perception and less regulatory scrutiny.

Telefonica’s 2021 assessment identified water management as material only from an impact perspective, while physical climate change impacts were material solely from a financial perspective. Energy and emissions management, employee health and safety, and cybersecurity registered as material from both vantage points.

Companies should allocate at least three months to complete their double materiality assessments when dealing with numerous stakeholder groups. It is wise to start the preparation early so that collaboration across different departments like legal, audit, finance, and operations is smoother, and they can all understand what the strategic implications are.

First, set up the frameworks for governance before you start your assessment. Since there are multiple departments involved in the process, to avoid any confusion or delay, you should assign a project manager responsible for coordinating implementation and requirements across departments. Your highest governance body, for example, a CEO or a managing director, should oversee the process and approve final material topics. Companies with robust sustainability teams may manage assessments internally, while others engage external consultants to add credibility and facilitate candid stakeholder feedback on controversial topics.

Begin by identifying upstream processes, including raw material origins and suppliers, then examine downstream activities covering customers, distribution channels, and end-users. Your value chain extends beyond direct operations to business relationships where impacts, risks, and opportunities frequently occur, such as collaborations with suppliers and partnerships with distributors that can enhance efficiency and market reach. Create a stakeholder profile capturing each actor’s size, sector, location, and activity nature.

The number of stakeholder groups varies based on the size and complexity of each company and its industry. For example, for a smaller company, you should engage 4–8 stakeholder groups, whereas for larger companies, the number increases to 15 or more. In any case, it is important to maintain focus without overwhelming your project scope. Most common groups involve employees (usually separated in management and stuff), customers, investors/shareholders, suppliers, financial institutions, local communities, NGOs, distributors, media, and other partners (media, technology, etc.).

Stakeholders give their opinions through surveys and further discussions, and then consultants or sustainability teams analyze the feedback so that the company can evaluate and keep the most important issues for decision-making.

Assess negative impacts using three criteria: scale (severity to people and environment), scope (geographical and demographic reach), and irremediability (whether harm can be reversed). For potential impacts, factor in likelihood of occurrence. Document both actual impacts already occurring and potential impacts that could materialize across short, medium, and long-term horizons.

Evaluate financial materiality based on magnitude (size of financial effects) and likelihood (probability of occurrence). Consider revenue reductions, increased operating costs, capital expenditure changes, regulatory fines, reputational effects, and access to capital with favorable terms. Financial risks and opportunities often emerge from impact materiality over time.

A consistent scoring system that combines numbers and expert judgment helps the prioritization of material topics. As mentioned earlier, companies usually rank topics by comparing their importance to each other and may measure risks and opportunities more precisely over time. They also set minimum importance levels for both business and societal impacts. If a topic passes either level, it must be reported under CSRD rules.

The list of possible ESG topics should be relevant to the business, and they are selected from industry standards and reporting frameworks, regulations, and stakeholder concerns, while examples also include climate change, employee safety, data privacy, supply chain labor practices, and waste management.

Next, a chart called a materiality matrix shows in a visualized way what the most significant sustainability topics are to the business and the stakeholders accordingly. Usually, the x-axis shows how important the topics are for financial materiality, and the y-axis shows how important they are for impacting society and the environment.

Topics in the top right quadrant are the most important, coming from both the stakeholder and business points of view. There should be documented reasoning for the barrier to be clear, which will help with auditing.

After the double materiality assessment is completed, the company holds a roadmap that serves the mandatory process and acts as a guide for the company to approach ESG more strategically in relation to its activities.

The mapping of material impacts, risks, and opportunities to corresponding disclosure requirements and data points within relevant topical standards determines the information your company must disclose. Maintain detailed documentation of management decisions and outcomes for each material topic, as capturing judgments throughout the process supports assurance requirements. Integrate material topics into your corporate planning cycles, budget allocations, enterprise risk management frameworks, and product development pipelines. Assign functional ownership for each material topic to departments like Finance, Operations, or HR, with your sustainability team coordinating integration rather than owning execution.

Your sustainability report communicates environmental, social, and governance impacts to stakeholders who assess risks and opportunities your company faces. The report serves as a communication tool demonstrating sincere action to skeptical observers. Develop clear reporting and communications strategies addressing multiple stakeholder audiences through appropriate channels, such as social media, newsletters, and stakeholder meetings, to ensure that all relevant parties receive timely and accurate information about your sustainability efforts.

Material topics might not be of the same importance each year. A company must review its double materiality assessment annually to ensure relevance. For example, when material changes occur in organizational structure or when external factors create new impacts, risks, and opportunities, there should be an update. Social factors and stakeholder expectations change rapidly, requiring regular reviews to prevent outdated reporting, especially in response to evolving societal norms, regulatory changes, and shifts in consumer behavior.

If there is anything that professionals now starting with ESG should keep in mind, it is that materiality is not only a reporting requirement. It is a practical way to understand how sustainability connects to their business performance and the real-world impact. By following a clear and structured process, even beginners can identify what truly matters, make better decisions, and build a stronger and more resilient strategy.

Most importantly, double materiality helps you move from simply reporting sustainability to actually managing it, ensuring your company is prepared for regulatory expectations while creating long-term value for both the business and society.